On June 1st, Cambridge, Massachusetts began accepting applications for its Rise Up program marking the beginning of a new phase in the modern guaranteed income movement. The program will provide $500 a month for eighteen months to all Cambridge families with children under the age of 21 who earn at or below 250% of the federal poverty level. The key word being all.

Up until now, municipal guaranteed income pilots across the country have been lottery-based, primarily because of limited funding. These programs, like the Cambridge RISE program that paved the way for Rise Up, are making vital contributions to our understanding of how no-strings-attached cash assistance impacts various populations, and have pushed the idea of guaranteed income into the mainstream. In pilot after pilot, we’ve seen how guaranteed income stabilizes families’ finances and increases their ability to weather financial shocks, improves recipients’ mental and physical health, and empowers families to make the choices that are right for them. As Cambridge Mayor Sumbul Siddiqui said in announcing the new program, “With Rise Up, we’re building off the tremendous positive impact we saw from the Cambridge RISE pilot, which showed us how far $500 a month goes toward establishing financial stability for families and creating better outcomes for our kids. There is no better investment we can make as leaders than in our families.”

Cambridge will be using $22 million of their American Rescue Plan Allocation to fund the project, about a quarter of their total ARPA allocation. The once-in-a-lifetime federal funding certainly has contributed to Cambridge’s ability to experiment with guaranteed income in this way. Additionally, Cambridge has the advantage of having a relatively small percent of low- and moderate-income residents. 12.3% of Cambridge’s population, and 7.4% percent of its families, live below the poverty line. In the District of Columbia, those numbers are 16.5% and 11.6%, respectively. Cambridge’s median household income is $112,565, compared to $93,547 in D.C, suggesting a considerably higher income distribution. Still, if the District had chosen to use a quarter of its ARPA allocation this way – about $825 million – it could have provided 18 months of income to over 75,000 individuals – enough to provide $9000 over 18 months to every District household receiving SNAP benefits, for example.

That said, ARPA funding is time limited. Programs funded this way leave open the question of how or if they will continue after the federal funding runs out. In the District, there is another option that could make D.C the first city in the country to offer a guaranteed income program as an entitlement to all its impoverished residents. The District could implement a mansion tax – a surcharge for residential properties in the top 2% of home values – and use the revenue to provide $500/month to families below the poverty line. Such a program would offer economic security to thousands of families, not a lucky few.

Economic Security Shouldn’t Depend on a Lottery

Our chances at economic security, Rise Up Cambridge reminds us, shouldn’t depend on winning a lottery. But far too often, it does. That lottery is most often the accident of birth. In the United States, the race, income, and wealth of the family you are born into are all strong predictive factors of the opportunities you will have to experience economic stability and mobility. The average white household, nationwide, has twice the income and ten times the wealth of the average Black household. In Washington DC, Black residents earn only one-third as much as white residents, and are five times more likely to live below the federal poverty line. Roughly 28,000 children, or 22.8%, in the District live in poverty. 85% of them are Black, while just 1-2% are white.

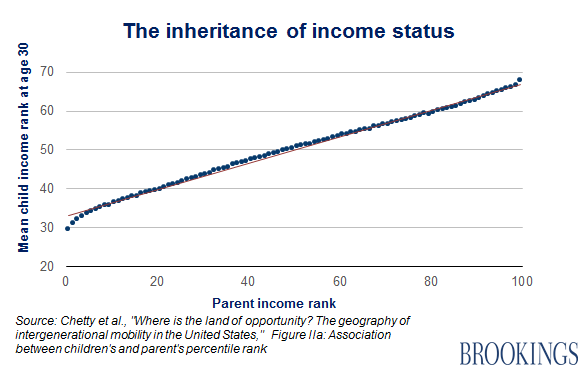

Because Black children are more likely to be born and raised in poverty, they are also far more likely to stay in poverty as adults. Extensive research has shown that children’s income as adults is strongly related to their parents’ income. Overall, only about 34% of children in the United States move into a higher income quintile than their parents. The lower your parents’ income, the harder it is to move up. Nearly half of children born to families with incomes in the bottom 20% will remain in the bottom 20% as adults. Less than one in five will climb to the top two quintiles. Meanwhile, 39% of children born in the top quintile will stay there. And again, we see that when we factor race in, economic mobility becomes even harder and less common. 54% of Black children born to families in the bottom quintile will stay there. Only a quarter will make it to the top 60% of earners.

Source: Isaacs, Julia & Sawhill, Isabel & Haskins, Ron. (2008). Getting Ahead or Losing Ground: Economic Mobility in America. Brookings Institution.

There are a long list of reasons for this economic “stickiness,” including access to high-quality educational opportunities, access to better health care, social capital and connections, exploitative systems that drain wealth from low-income households, and, of course, an economic and social order built on white supremacy. Crucially, none of these reasons are inherent. There doesn’t have to be a system that keeps poor families poor and rich families rich. Our economic well being doesn’t have to be contingent upon the birth lottery. That is just the choice we’ve made.

Guaranteed Income Should be a Targeted Entitlement

A better choice starts with recognizing a simple truth: the path to economic stability and mobility starts with cash. Research has shown time and again that providing low-income individuals and families with no-strings-attached cash has enormous benefits. Over the long term, researchers have found that an extra $3,000 in a family’s annual income when a child is younger than age 5 leads to 19% higher future earnings. Other studies have shown that increasing family incomes has tangible outcomes on education, health, and incarceration. Higher family incomes mean higher graduation rates from high school and college and improved health outcomes for infants and mothers. Cash assistance has been linked to lower rates of arrest. A pilot study in Canada found that giving $7500 CAD (approximately $5800 USD) to those experiencing homelessness helped recipients move into stable housing faster, spend fewer days in shelters, and save over $1,000 over 12 months. Another study found that when mothers with low incomes received just over $300 in monthly cash assistance during the first year of their children’s lives, it literally changed their babies’ brains. Their infants’ showed significantly more brain activity associated with higher language and cognitive scores and better social and emotional skills in children as they grow older.

Our recent national experiment with the Child Tax Credit provided further evidence that cash assistance is key to families’ economic well being. Indeed, the monthly CTC, which functioned as a temporary guaranteed income for all but the highest-earning families, cut childhood poverty nearly in half, decreased families’ reliance on high cost financial services (like payday loans), and meaningfully reduced evictions among recipients, among many other benefits. Not only do these outcomes ease families’ hardship in the short run, but they also interrupt cycles of poverty that low-income families can become trapped in, both in the short term and across generations. Evictions, payday loans, and childhood poverty (as we discussed above) are not just the results of today’s economic instability, but are drivers of tomorrow’s. By interrupting these cycles, guaranteed income can make economic stability more than a lucky break. But, as Cambridge has reminded us, it shouldn’t just create a new lottery for families to win or lose. Instead, guaranteed income should be an entitlement that all low-income families in America can rely on.

Washington D.C., with its extreme concentrations of wealth and income inequality has the resources to make this a reality. Approximately 16,500 households in the District have incomes under 100% of the FPL ($30,000 for a family of four in 2023). To provide each household with a $500/month guaranteed income would cost approximately $100 million a year in direct costs. Of course, every program has administrative costs. So, let’s assume an additional 10% for overhead. The total cost of such a program would be $110 million.

$110 million is a lot of money – sort of. Such a program would cost only a fraction of the cost of any of the four proposals outlined in the District’s own report on providing a minimum income. The lowest cost option they considered would require $380 million a year. That option would create a refundable tax credit that would function to create an income floor equal to 100% of the Federal Poverty Level to all District households. That, is of course, an advantage of that plan. That said, providing $6000 a year to a family of three earning 50% of the federal poverty level would represent a 50% increase in their income. It would lift many families earning below the poverty level above it. It would provide significantly more support to almost all low income families than either Councilmember Parker’s District Child Tax Credit proposal or his Financial Support for Families with Children plan.

Moreover, in the context of the District’s $19.7 billion FY24 budget, $110 million is a vanishingly small number: only half of one percent of the total. Of course, the District’s budget includes quite a lot of revenue from the federal government or revenue that must be used for specific programs – only $9.7 billion is made up of local general funds. $110 million is just over 1% of that. However, let’s assume for the moment that every dollar of that $9.7 billion is going to valuable programs and services that we want to preserve. Where could we find $110 million for this guaranteed income program?

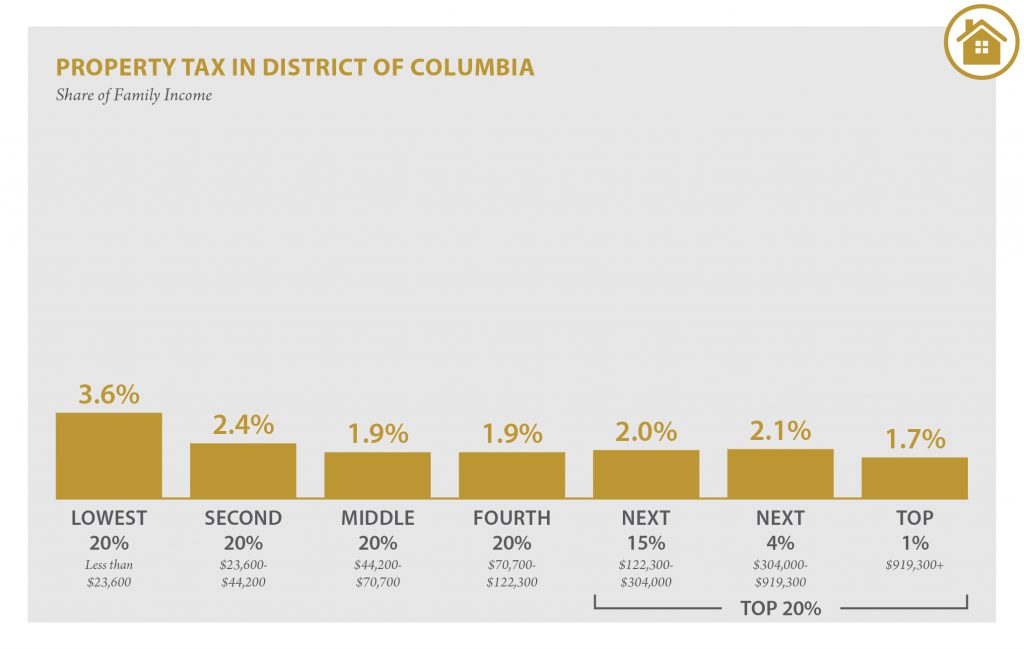

Here’s one answer: the District could implement a mansion tax. The District’s tax payers pay far lower real estate taxes than in any of the surrounding jurisdictions. Moreover, the District’s residential properties are taxed at one flat rate, meaning they fall most heavily on lower-income residents. Importantly, renters, who are generally lower-income than home-owners, also pay property taxes, indirectly, through their rent. As the table below shows, the bottom 20% of earners are paying more than twice of their family income in property taxes than the top 1%.

Source: Institute on Taxation and Economic Policy, Who Pays? Sixth Edition. District of Columbia (2018).

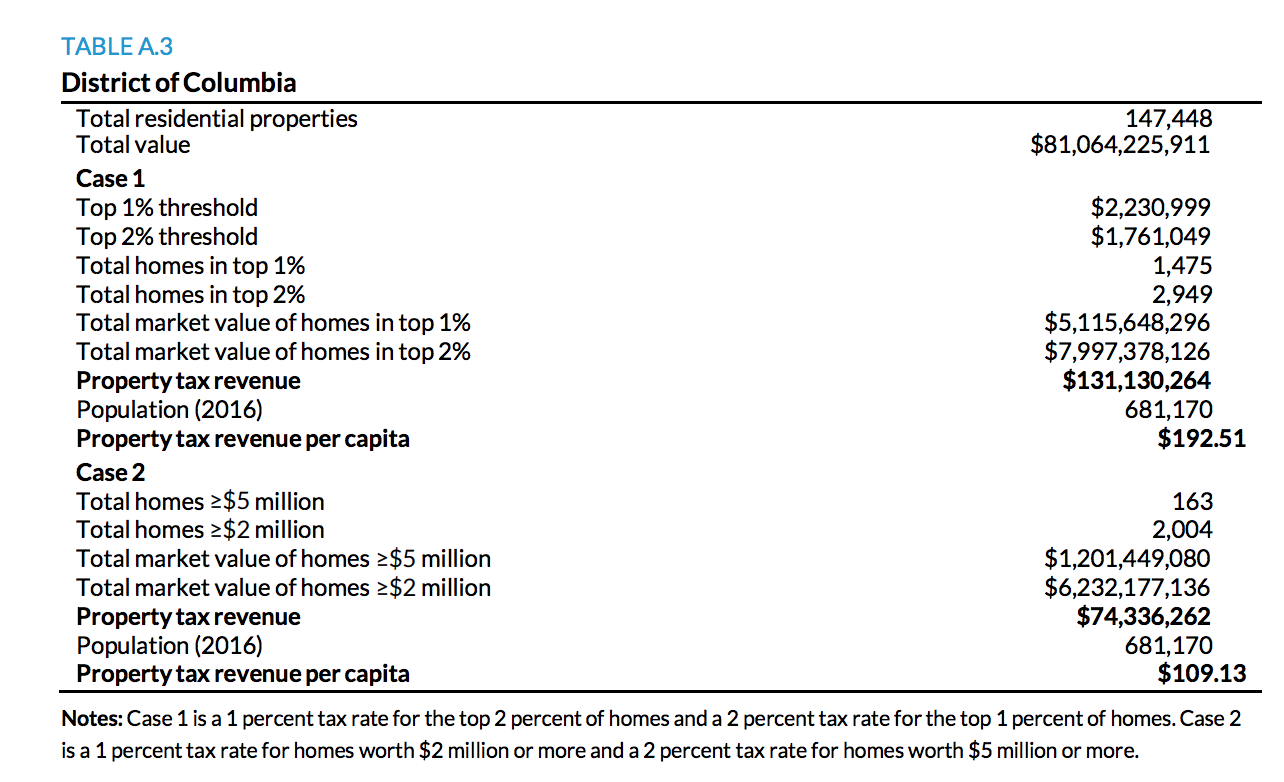

To move towards fixing this inequity, the District could tax homes in the top 2% of assessed values at a higher rate. Though no states have yet implemented such a tax policy, New York and Rhode Island have considered similar proposals, and several states tax the highest-value home sales at a higher rate than other residential real estate transactions. In 2018, The Urban Institute did a detailed analysis of the impact of such a policy. Such a tax would affect about 3,000 residential properties, all with 2018 values over $1.7 million. The policy would levy a 1% tax on properties in the top 2% of market values, and a 2% tax on properties in the top 1% of market values. The analysis found that the District would bring in $131 million annually from this policy. Of course, it’s no secret that home values have significantly increased since 2018. It is likely that, if implemented today, a mansion tax would result in even more revenue for the District.

Source: Urban Institute, “Exploring the Viability of Mansion Tax Approaches,” 2018.

With the revenue from this new tax, the District could fund a District-wide, sustainable guaranteed income program that would reach all households living under the poverty line.

The impact would be monumental. Children would be better fed, have more stable homes, and would get better healthcare. Their parents would be physically and mentally healthier. More students would graduate from high school and college. Arrests in the District would fall. And a real shot at financial stability and mobility would be the birthright of every District resident, not a prize reserved for the lucky few who win a lottery.